All suppliers are used to creating invoices in GST quite often. But there are situations when you have already issued an invoice, yet your client is not happy there is a discordance in your invoice. In some cases, the client returns some goods and you will have a negative impact on your accounting balance so you will have to issue a credit note. In other cases, a client receives goods in excess so you need to issue a debit note. Let’s explore what is a credit note and what is a debit note and the specific details on when to issue one or the other.

What is a credit note?

As mentioned, when there are issues with the goods or services supplied to a client and they return goods, or there is a discordance in the invoice, the supplier has to issue to the recipient a credit note using a gst compliant billing software.

When to issue a credit note?

A credit note should be issued in of these cases:

When some are all goods supplied have been returned by the client.

When services or goods provided to your client have been deficient.

When the quantity received by the client is less than the one that appears on the issued tax invoice.

When the supplier has added a higher tax rate that the actual amount of tax that needs to be paid for the goods or services provided to the client.

When the supplier has created an invoice with a value greater than the actual value of the goods or services provided.

The credit note needs to be declared in the GSTR report corresponding to the correct month.

What is the meaning of debit note?

An invoice is raised on every supply of goods or services. When the supply of such goods or services is different than the contents of the invoice due to certain conditions, or extra goods have been delivered to the recipient, then the seller needs to issue a debit note. This debit note will reflect the upward revision of prices in an already issued invoice and will serve to the recipient of goods / services of any future liability that they have to pay.

When to issue a debit note?

A debit note can be issued in any of these cases:

The original tax invoice has already been issued and the taxable value on the invoice is less than actual taxable value.

The original tax invoice has been issued and the tax charged in the invoice is less than the actual tax that should be paid.

What is the credit note / debit note format?

Based on the GST rules and guidelines, a credit / debit note should contain:

Name, address and GSTIN of supplier

Name: credit note or debit note

A unique serial number for the current financial year

Date of issue

Name, address, GSTIN (or UIN in unregistered) of recipient

Serial number and date of the corresponding tax invoice (or bill of supply)

The taxable amount of goods or services, the rate and amount of tax that is credited or debited to the recipient

Signature or digital signature of the supplier, or of an authorized representative

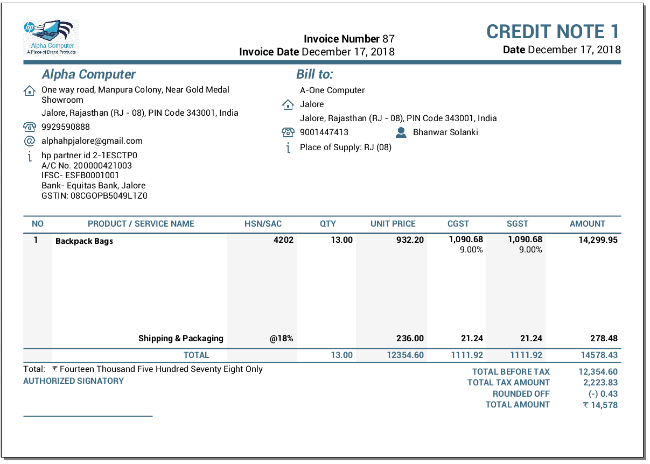

This is how a credit note made with Sleek Bill looks like:

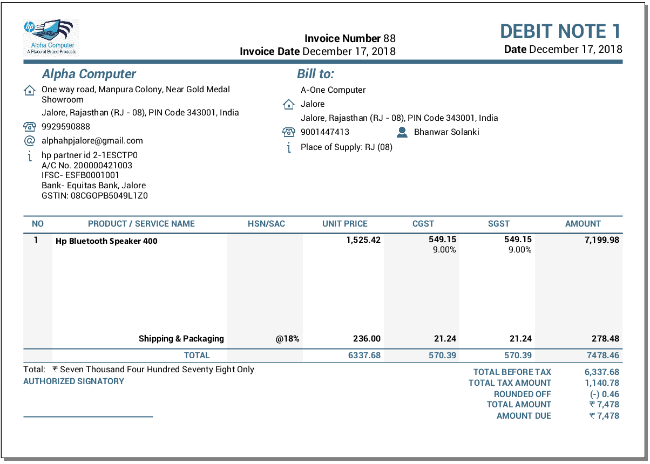

This is how a debit note made with Sleek Bill looks like: