Delving into the Unique Features of the Composition Scheme The Composition Scheme, a facility for taxpayers of small business in the Goods and Services Tax (GST) regime, is an uncomplicated and handy choice. This scheme aligns with our billing software's dedication to deliver expert, authoritative, and reliable information – it guarantees that managing your GST compliance becomes easy while maintaining precision.

The Composition Scheme is open to small taxpayers who have a yearly turnover below Rs. 1.5 crore. This threshold of turnover makes the scheme accessible to a significant number of small businesses, simplifying their GST formalities.

Purpose of the Composition Scheme

The main aim of the Composition Scheme is to minimize the weight of difficult GST formalities on small taxpayers. When businesses choose this scheme, they can pay GST at a set rate according to their turnover, which makes the tax payment procedure simpler .

Fixed Rate on Turnover: Simplifying Compliance

Composition Scheme means that taxpayers must pay a fixed GST rate on their turnover. This method greatly simplifies compliance, benefiting small businesses in managing their GST responsibilities.

Opting into the Composition Scheme

Tax payers who are eligible have the right to select the Composition Scheme according to their requirements and choices. This decision should be in line with business operations and financial aims.

Verify with the GST Search Tool

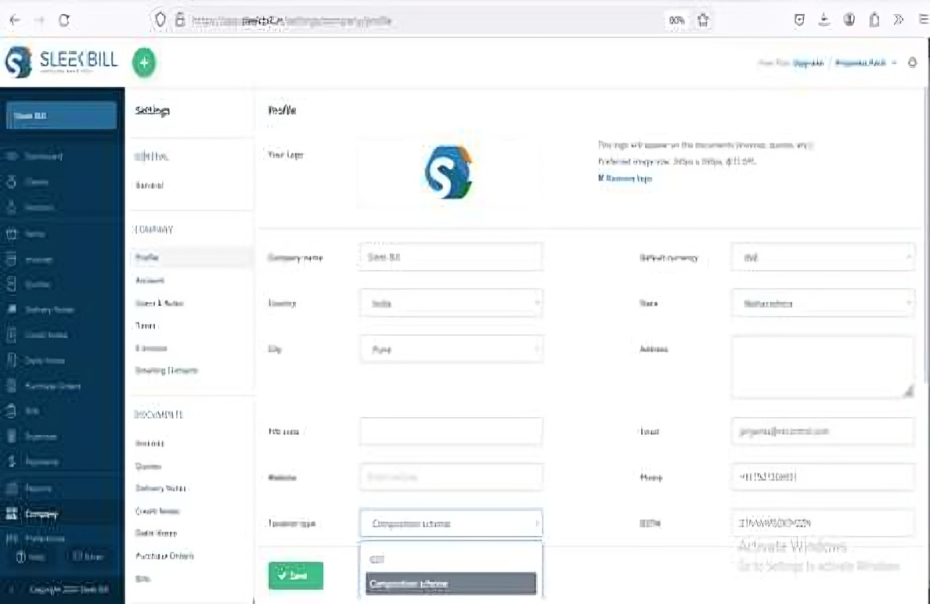

The tool to search GST is a good way for you to confirm if a taxpayer falls under the Composition Scheme or not. Just search are they regular taxpayers, or under the Composition Scheme by seeing in which 'Taxpayer Type' column their name appears.

GSTIN Verification

For validating the business's participation in Composition Scheme, use GST Identification Number (GSTIN) to search in GST tool. This will provide information about their taxpayer type and confirm if they are part of the Composition Scheme.

Ease of GST Formalities

For small taxpayers enrolled in the Composition Scheme, the difficult GST formalities that regular taxpayers face are significantly reduced. This simplification is a key advantage for small businesses, making GST processes more manageable.

Standard Limit: Businesses with a turnover below Rs. 1.5 crore are eligible for the Composition Scheme.

Special Consideration for Certain States: For businesses in North- Eastern states and Himachal Pradesh, the turnover limit is lower, set at Rs. 75 lakh.

Enhanced Range for Service Providers: Dealers of composition can provide services that are up to 10% from their turnover or Rs. 5 lakhs, based on which one is more as stated in the CGST Amendment Act from year 2018.

Effective Date: This amendment has started applied force from 1 February 2019.

Instructions for Service Providers: In the 32nd meeting of the GST Council, it was inform to increase the threshold limit for service providers.

Awaiting Details: The exact details about this suggested rise were not given in the initial content.

Basic of Aggregate Turnover : We should use the aggregate turnover as a basis to decide eligibility, because it includes all businesses under the same PAN in this calculation.

Turnover in Composition Scheme : This method is complete and it helps businesses to measure their fitness according to the full turnover. It makes it simpler for them to follow the conditions of this scheme.

Taxpayers who fall into these categories cannot choose the Composition Scheme under GST.

● Specific Product Restrictions:

Manufacturers of ice cream, pan masala, or tobacco products are excluded from the Composition Scheme.

● Reason for Exclusion:

These industries are often subject to different tax structures and regulatory considerations.

● Cross-State Supply Limitation:

Businesses involved in inter-state supplies (supplying goods or services across state boundaries) are not eligible for this scheme.

● Rationale:

Businesses involved in inter-state supplies (supplying goods or services across state boundaries) are not eligible for this scheme.

● Casual Taxable Person:

Those who conduct transactions occasionally in a state or union territory where they have no fixed place of business are considered casual taxable persons.

● Non-Resident Taxable Person:

Individuals who reside outside India but supply goods or services to a India region .

The Composition Scheme in GST gives a straightforward tax system for small businesses. But, there are some requirements that the business must meet to use this scheme:

● Reverse Charge Mechanism:

Taxpayers under this scheme must pay tax at normal rates for transactions under the Reverse Charge Mechanism.

● Business Premise Display:

Taxpayers must prominently display 'composition taxable person' on their business premises.

● ITC Restriction:

Businesses opting for the Composition Scheme cannot claim Input Tax Credit on their purchases.

● Inclusion in Bills:

This status must also be mentioned on every bill of supply issued.

● Expanded Scope:

After the CGST Amendment Act 2018, effective from February 1, 2019, manufacturers or traders in the Composition Scheme can also supply services up to 10% of their turnover or or Rs. 5 lakhs, whichever is higher.

● Collective Scheme Adoption:

If a person owns multiple business segments under one PAN, they must register all these businesses collectively under the Composition Scheme or choose regular GST compliance for all.

● GST-Applicable Goods Only:

Dealers must only supply goods taxable under GST. Non-taxable goods, like alcohol, are not allowed under this scheme.

There is few steps initially you have to follow set your business in Composition Scheme in taxiation type before start making invoice.

The Composition Scheme in GST made tax management easier for small businesses. Here are the steps a taxpayer can take to choose this scheme:

Composition dealers, who opt for a simplified tax scheme under GST, have specific guidelines for billing:

*Free & Easy – no hidden fees.

| Type of Business |

CGST Rate |

SGST Rate |

Total GST Rate |

|---|---|---|---|

Manufacturer and Traders (Goods) |

0.5% |

0.5% |

1.0% |

Restaurants not serving alcohol |

2.5% |

2.5% |

5.0% |

Other Service Providers* |

3.0% |

3.0% |

6.0% |

*Note: The inclusion of "Other Service Providers" in the Composition Scheme and the associated rates were proposed in the 32nd GST Council meeting, but a formal notification is yet to be issued for this inclusion.

The Composition Scheme in GST is benefesial for small and medium enterprises (SMEs) in many ways.

Simplified Tax Structure: This scheme simplifies the tax framework, significantly lowering the compliance requirements for businesses.

Fewer Return Filings: Composition dealers need to file fewer returns, making the GST process hard and time-consuming.

.png)

Tax Rates That Are Beneficial: The pattern allows for taxation at a set rate depending on turnover, resulting in lower tax responsibility comparatively.

Regular Tax Rates: The fixed-rate arrangement provides stability and predictability to businesses, allowing for better planning of financial matters. This aids in more effective financial planning and budgeting.

Boost in Liquidity: Lower tax rates under the Composition Scheme make a business's overall liquidity stronger. Increased Retained Earnings: Businesses have the ability to keep a bigger part of their earnings when they pay lesser tax, which increase the overall cash flow and financial standing of any business. GST Payment Guidelines for Composition Dealers

Boost in Liquidity: Lower tax rates under the Composition Scheme Enhanced a business's liquidity.

More Money Kept: The business can keep more of its money if it pays less tax, which assists in enhancing liquidity and potential growth.

Self-Payment Obligation: You need to pay GST directly from your own funds for the supplies you make, as you cannot collect GST from customers.

GST on Own Supplies: This includes the GST due on the supplies made by you.

Tax on Reverse Charge Transactions: Also includes tax payable under the reverse charge mechanism on certain transactions.

Possible Tax Payment: You might need to pay taxes for buying from dealers who aren't registered.

Date of Implementation : Starting February 1st, 2019, people must pay taxes when buying from dealers who aren't registered.

Notification Dependent: The applicability of tax on purchases from unregistered dealers depends on the future notification of specified goods and services, and the class of registered persons. Until such a notification is issued, this tax may not apply.

Knowing about the requirements for filing GST return is necessary for dealers who fall under composition scheme. Here are things you should know:

● Quarterly Payment Requirement: Use CMP-08 to pay taxes quarterly. ● Submission Deadline: CMP-08 should be filed by the 18th of the month following the quarter’s end.

● Annual Return Form: File your annual return TAX using GSTR-4. ● The Filing Deadline: For GSTR-4, File return the deadline is on 30th April of the new financial year starting from FY 2019-20.

.png)

● GSTR-9A Filing: You need to submit this tax form every year before December 31 of the following year. ● Waiver for Perticular Years: The need to submit GSTR-9A was waived for the financial years 2017-18 and 2019-20.

● Filing Requirement Waived: You don't have to file GSTR-9A for certain financial years, like FY 2017-18 and FY 2019-20.

● Simplified Documentation: Composition dealers are exempt from maintaining detailed records, easing their documentation burden. ● Seller Notification: Sellers receive email notifications for record-keeping.

Let's talk about the good and bad sides of the GST Composition Scheme, which helps small businesses but also has its pitfalls:

● Ineligibility for ITC: One of the major drawbacks is the inability of composition dealers to claim Input Tax Credit. This means they cannot offset the GST paid on inputs against their sales tax liability.

● Financial Impact: The lack of ITC can affect the cost-effectiveness and pricing strategies of businesses, especially those with significant input costs.

● Geographical Limitations: Composition dealers are limited to conducting business within their state and cannot engage in inter- state transactions.

● No E-commerce Sales: Dealers under this scheme are also prohibited from selling goods through e-commerce platforms.

● Non-Taxable Goods: Composition dealers are not allowed to deal in goods that are non-taxable under GST, like alcohol.

● Service Limitations: There are also restrictions on the types of services they can provide.

● Transactional Limitations: Dealers may find themselves ineligible to participate in certain types of transactions or business models, which can limit their market opportunities and scalability.

Ignite Your Business: Explore the Transformational Power of the GST Composition Scheme

FREE SIGN UP NOWFree or Premium - no hidden fees.